I wrote this blog post in 2017, new comments in 2023 (6 years later) written in red font.

In 2017, US stocks doubled in last 5 years

The S&P index is up 16%+ year-to-date. A good thing right? One fund manager recently commented that investors have never been so grumpy, while making great returns. This is the “Wall of Worry” – so many things to worry about, which oddly, have not affected the markets’ willingness to go higher. Yes, people are getting richer, and yes, it’s kind of exhausting. It keeps climbing higher, for now.

So much to worry about

Crazy talk on the news daily, Federal Reserve tightening money supply, hurricanes, anti-trade populist sentiment, mass shootings, Russian interference with US elections, etc. . . I dare you to check your news feed. . . the ratio of negative (or useless) fluff to real news is 8:1.

No matter. Stocks going higher

For those of you who have money in the US market through your 401K plan at work or personal investments, times are good. After all, it’s been a great run for the last several years. 16% on 2012, 32% in 2013, 13% in 2014, 1% in 2015, 12% in 2016. Amazing, the broader market has doubled in 5 years.

In November of 2023 (6 years) later, the SPY is at 455. . .more than double. So, basically this has doubled twice in the last 10 years or so. That is incredible. We in the United States are so lucky to be a part of, investing in, the most dynamic economy, hub of innovation, and profit-making machine in history. Go, go, go.

Stock price = earnings x multiple

On some level, the price of stocks is driven by earnings (how much money companies are making), and the P/E multiple (how much investors are willing to pay for the same $ of earning). Earnings have been good with 70%+ of companies in Q3 beating Wall Street analyst estimates. Tons of companies are doing great – Home Depot, Walmart, Square, Boeing, Facebook, Netflix – and you hear that dozens of companies are setting new all-time highs every week.

Why are earnings so good?

Some call it a synchronized global recovery with US, Europe, China doing well. Others call it a weak dollar and excess liquidity (read: quantitative easing) because interest rates have been super low for almost 10 years. Look that chart of the 10-year yield for the last 40 years.

If anyone tells you that the competitive landscape is harder now than it was in the 1980s, you can point them to this interest rate chart and give them a moment for pause. The previous generation of business leaders had to deal with 10-15% hurdle rates in their business, while we only have to deal with 2-3%.

Price multiples

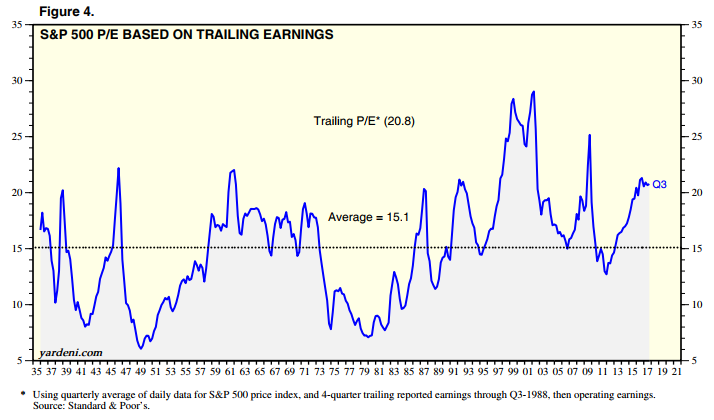

Are investors more willing to give a higher P/E multiple to stocks? Definitely. Take a look at this chart below from Ed Yardeni here. I don’t claim to understand this entirely, but the gist of the story is that P/E multiples expand when interest rates are low (less competition for investment dollars) and inflation is low (higher quality earnings). Looks like the median P/E multiple in the S&P for the last 80 years has been 15. Currently, it’s at 21.

Are you a net-buyer of stocks?

This is the farthest thing from an investment blog, so definitely consult your financial adviser. That said, for me, it depends on your investment time frame. I still have quite a while until “retirement” (able to withdraw from a Roth IRA or 401K without penalties), so I am a net buyer of US equities. For me, it’s good when strong stocks go on sale.

Stay invested

Tony Robbins notes in his recent book, MONEY: Master the Game, (affiliate link), that timing the stock market is crazy difficult. In a recent study the average CAGR for the US stock market was 8.2% – not bad. However, if you missed the top 30 trading days. . . that’s 30 / 2,400 days = 0.6% of the best performing days, you had a negative return. Crap. Are you smart enough to not miss the best 0.6% of trading days?

Update from the future (2023); interest rates have been raised 11 times over the 3 years. The fed funds rate went from 0.25-0.50% now to 5.25-5.5%. . . 500 basis points. That makes debt a LOT more expensive. So still stay invested in your are young and can afford (read: benefit from) the volatility? Probably yes. I am.

Net-Net. US stocks are grinding higher

Immune from the crazy talk from Washington, threats from N Korea, mass shootings, natural disasters, and Fed tightening. Stocks are climbing the wall of worry. For those of us investing for the long-haul and dollar-cost averaging, see you 20-30 years later.